How Established Businesses Are Stacking $500K+ in Unsecured Capital Starting at 0% Interest (2026 Guide)

The complete playbook for business owners with 2+ years in business, $1M+ revenue, and 720+ FICO who are ready to deploy serious capital — without giving up equity, posting collateral, or paying double-digit interest.

TL;DR — Key Takeaways

- ✓$500K+ in unsecured capital is accessible at 0% interest for qualified established businesses — no collateral, no equity dilution.

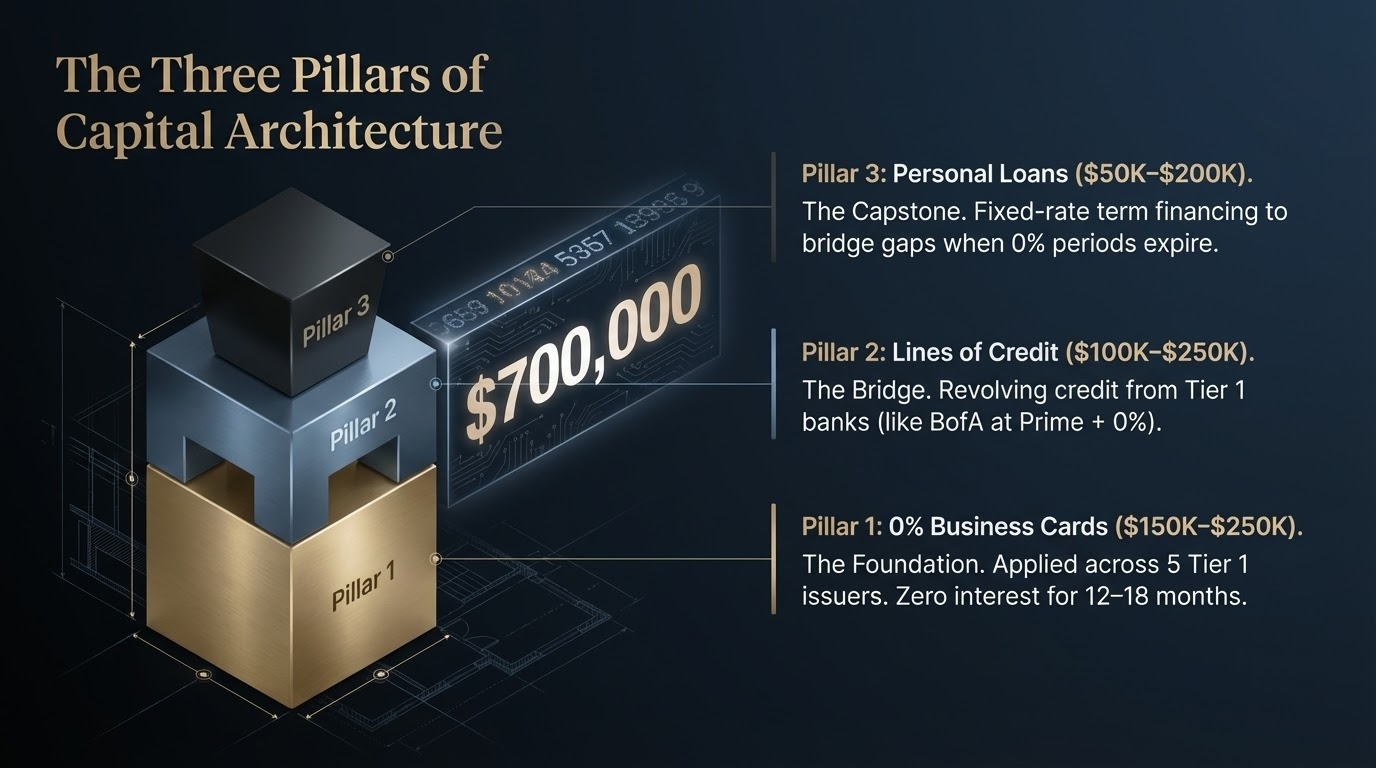

- ✓The strategy uses a three-pillar approach: 0% APR business credit cards ($150K–$250K) + business lines of credit ($100K–$250K) + personal loans ($50K–$200K).

- ✓The refinancing cycle keeps capital costs near zero perpetually — you're never forced to pay off the stack, just rotate it.

- ✓Requires a "bankable" profile: 720+ FICO across all bureaus, 2+ years in business, $1M+ revenue, and existing Tier 1 bank relationships.

- ✓The US Bank Business Shield Visa at 18 billing cycles (in-branch only) is the anchor product of any serious capital stack in 2026.

- ✓Most business owners only access 10–20% of their available credit capacity — this guide shows you how to access the other 80–90%.

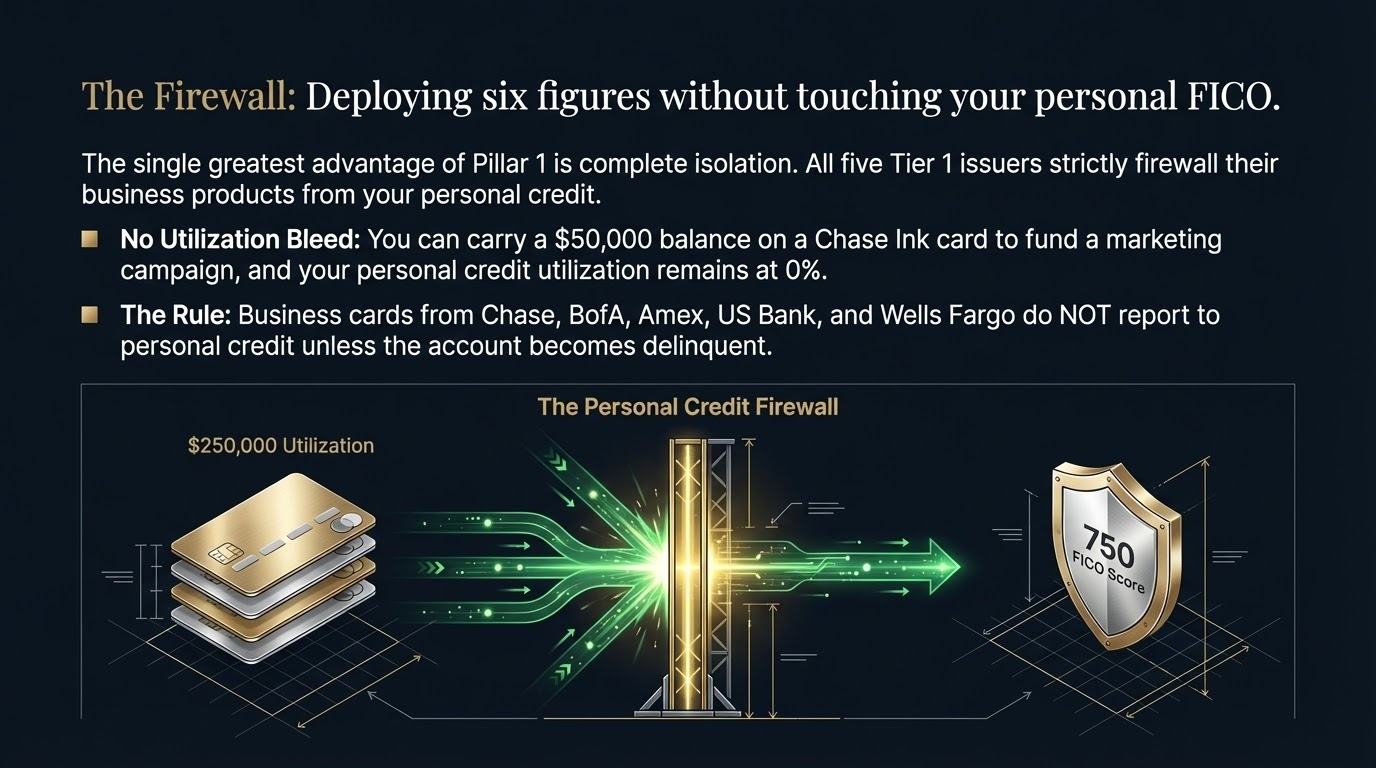

- ✓All five Tier 1 issuers — Chase, BofA, Amex, US Bank, and Wells Fargo — do NOT report business cards to personal credit (unless delinquent). This is a major advantage of business credit stacking.

The Capital Architecture Framework

Most business owners think about funding one product at a time: "Should I get a business credit card?" or "Should I apply for a line of credit?" That's the wrong mental model. Capital architecture is about engineering an interlocking system of credit products that collectively give you access to half a million dollars or more — at effectively zero cost, for as long as you need it.

The three-pillar capital stack works because each pillar serves a different function and draws from different credit capacity:

Together, these three pillars can put $300K–$700K of working capital in your hands at costs ranging from 0% to 7–12% — a dramatic improvement over the 25–50%+ effective rates most businesses accept from MCA lenders or short-term loan providers. According to Bankrate's research on unsecured business loans, the average small business loan rate in 2026 sits between 6% and 45% depending on the lender — yet qualified businesses can access the same capital at 0% with the right strategy.

The prerequisite for this strategy is being what the banking industry calls "bankable" — a profile that qualifies for Tier 1 bank products. This isn't a strategy for startups or businesses with credit challenges. It's for established business owners who have already proven their business model and are ready to scale with intelligent capital deployment.

Capital Architecture

Ready to stack your funding?

Our advisors map out the optimal combination of lending products for your business — from Chase to Amex to US Bank and beyond.

Book a Free CallPillar 1 — 0% APR Business Credit Cards ($150K–$250K)

The foundation of every capital stack. Applied strategically across five Tier 1 issuers, you can access $150,000–$250,000 in credit limits at 0% interest for 12–18 months per card.

Chase Ink Business Cards — 0% for 12 Months

Chase is the starting point for any capital stack. The Chase Ink family offers two cards with 0% intro APR periods that are tailor-made for business capital deployment. Chase typically approves $15,000–$50,000+ per card for qualified applicants, meaning a single issuer can put $30,000–$100,000 in your hands at zero cost.

- → Ink Business Unlimited®: 0% intro APR for 12 months (then 16.74%–24.74% variable), $0 annual fee, unlimited 1.5% cash back on all purchases, $900 cash back bonus after $6,000 spent in the first 3 months. Per NerdWallet's 0% business card analysis, this is among the strongest no-fee 0% offers available.

- → Ink Business Cash®: 0% intro APR for 12 months (then 16.74%–24.74% variable), $0 annual fee, 5% cash back on office supplies and internet/phone/cable services (up to $25,000 combined annually), $900 cash back bonus. The rewards structure makes this ideal for businesses with high utility and telecom spend.

For established businesses, I always start with existing bank relationships. If you have a Chase business checking account, the Ink cards should be your first applications — relationship-based underwriting consistently produces higher initial limits. I've seen clients with strong Chase banking relationships receive $40,000–$75,000 per Ink card on their first application. Apply for both the Unlimited and the Cash on the same day — Chase counts both as a single hard inquiry when submitted together. That's two cards, one pull. Chase pulls Experian, same as Amex and Wells Fargo. BofA and US Bank both pull TransUnion, making them your second bureau pair.

Credit reporting: Chase business cards do not report to personal credit bureaus unless the account becomes delinquent. Applications pull Experian in most states. Chase and Amex form your Experian pair in Round 1, while BofA and US Bank form your TransUnion pair — two pulls per bureau, then you pause to remove inquiries before the next round.

Bank of America Business Advantage Cards — 0% for 7 Billing Cycles

Bank of America offers four distinct business credit cards, all with 0% intro APR for 7 billing cycles. While 7 billing cycles is shorter than Chase's 12 months, you can hold multiple BofA cards simultaneously — and BofA's Preferred Rewards for Business program can meaningfully boost your rewards rate if you maintain significant deposits with them.

- → Business Advantage Unlimited Cash Rewards: 0% for 7 billing cycles, then 16.74%–26.74% variable. $0 annual fee. Unlimited 1.5% cash back (boosted to up to 2.62% with Preferred Rewards Gold tier). $500 cash back bonus after $5,000 spend in 90 days.

- → Business Advantage Customized Cash Rewards: 0% for 7 billing cycles, then 16.74%–26.74% variable. $0 annual fee. Up to 3% cash back in a category of your choice (gas, travel, dining, online purchases, etc.). $500 cash back bonus after $5,000 spend.

- → Business Advantage Travel Rewards: 0% for 7 billing cycles, then 16.74%–26.74% variable. $0 annual fee. Unlimited 1.5 points per $1, boosted to 2.62 points with Preferred Rewards. 50,000 bonus points after $5,000 spend.

- → Business Advantage Platinum Plus Mastercard: 0% for 7 billing cycles, then 16.74%–26.74% variable. $0 annual fee. $300 statement credit (no rewards otherwise). Best for pure capital deployment with no rewards complexity.

BofA's Preferred Rewards for Business program is the best-kept rewards multiplier in business banking. If you're maintaining $100,000+ in combined BofA and Merrill accounts, you're at the Gold tier — which boosts your cash back from 1.5% to 2.62% on unlimited spend. But the real power move with BofA: you can hold up to 5 business credit cards, and all applications within a 30-day window combine into a single TransUnion inquiry. Your second approval is typically half of your first card's limit — apply until you're denied to maximize total credit. After approval, BofA allows you to combine all card limits into a single card if you want consolidated access.

Credit reporting: BofA business cards do not report to personal credit bureaus unless delinquent. Applications pull TransUnion, and all BofA applications within 30 days combine into a single inquiry. BofA allows up to 5 business cards — the 2/3/4 rule applies to consumer cards only, not business. If your TransUnion isn't looking ideal, freeze it and request BofA pull Experian instead.

American Express Blue Business Cards — 0% for 12 Months

American Express offers two 0% APR business cards that belong in every capital stack. Per Nav's 0% APR business card analysis, both Amex Blue Business cards combine 12-month 0% periods with strong rewards rates and $0 annual fees. Like the other Tier 1 issuers, Amex business cards do not report to personal credit bureaus unless delinquent — giving you the same utilization freedom as Chase and BofA.

- → Blue Business® Plus Credit Card: 0% intro APR for 12 months (then 16.74%–26.74% variable). $0 annual fee. 2X Membership Rewards points on all purchases (up to $50,000 per year, 1X after). Points transfer to airline and hotel partners — among the most valuable flexible rewards currencies.

- → Blue Business Cash™ Card: 0% intro APR for 12 months (then 16.74%–26.74% variable). $0 annual fee. 2% cash back on all eligible purchases (up to $50,000 per year, 1% after). $250 statement credit after $5,000 spend in 6 months.

If you already hold a personal Amex card for 3+ months, business card applications typically trigger only a soft pull — no hard inquiry impact on your Experian file. This makes Amex uniquely valuable in the capital stack: you get 0% capital without using up an Experian hard pull slot. Strategy: apply for Amex Blue Business cards first, before your Chase and Wells Fargo applications add hard inquiries to Experian.

Credit reporting: Does not report to personal credit unless delinquent. Amex pulls Experian — but here's the key advantage: if you already hold a personal Amex card for 3+ months, subsequent business card applications typically result in a soft pull only, meaning no hard inquiry on your Experian. This makes Amex the ideal first application before hard inquiries from Chase and Wells Fargo accumulate, or the ideal addition after inquiry removal on Experian.

US Bank Business Cards — The 18-Month Anchor

US Bank is the anchor of every serious capital stack in 2026. The reason: their US Bank Business Shield Visa offers an 18-billing-cycle 0% intro APR — the longest 0% period of any major business credit card — but only when applied for in branch. Online applications only receive 12 billing cycles. This single product can give a business 18 months of zero-cost access to a five-figure credit line.

- → US Bank Business Shield Visa®: 0% intro APR for 18 billing cycles (in-branch) or 12 billing cycles (online), then 16.24%–25.24% variable. $0 annual fee. 5% cash back on prepaid hotel and car rental bookings, 2% on qualifying purchases in the top two spend categories, 1% on everything else. New card in 2026. Per Upgraded Points, the in-branch 18-month offer is one of the strongest introductory APR products on the market.

- → US Bank Triple Cash Rewards Business Card: 0% intro APR for 12 billing cycles on both purchases and balance transfers (then 16.24%–25.24% variable). $0 annual fee. 3% cash back on gas/EV charging, office supplies, cell phone bills, and restaurants. Includes $100 annual software credit — offsetting $100/year of your SaaS spend.

- → US Bank Business Platinum Card: 0% intro APR for 18 billing cycles (in-branch) or 12 billing cycles (online), then 16.24%–25.24% variable. $0 annual fee. No rewards — pure capital vehicle. Ideal when you want maximum credit line without the rewards tracking complexity.

The US Bank Business Shield at 18 months is the anchor of any serious capital stack. Apply in-branch — I cannot stress this enough. Walking into a US Bank branch and applying with a banker will unlock the full 18-billing-cycle offer that you simply cannot get online. The difference between 12 and 18 months is six additional months of zero-cost capital — potentially worth thousands of dollars in avoided interest. US Bank typically pulls TransUnion — the same bureau as BofA. This means you pair BofA and US Bank on your TransUnion round, while Chase and Amex share the Experian round. Two pulls per bureau per round, then pause to remove inquiries.

Credit reporting: US Bank business cards do not report to personal credit unless delinquent. US Bank typically pulls TransUnion — the key bureau distinction that makes strategic stacking possible.

Wells Fargo Signify Business Cash — 0% for 12 Months

The Wells Fargo Signify Business Cash℠ Card rounds out the five-issuer card stack. It offers a straightforward unlimited 2% cash back rate — among the highest flat-rate business card returns available with no cap — combined with a 12-month 0% intro APR and a $500 cash bonus.

- → Wells Fargo Signify Business Cash℠: 0% intro APR for 12 months (then 17.49%–27.49% variable). $0 annual fee. Unlimited 2% cash back on all purchases — no categories, no caps, no enrollment required. $500 cash back bonus after $5,000 spend in first 3 months.

Credit reporting: Wells Fargo business cards do not report to personal credit unless delinquent. Wells Fargo pulls Experian — which means they pair with Chase and Amex on your Experian round. Wells Fargo allows up to 2 business credit cards, giving you additional 0% capacity from a third Experian-pulling issuer.

Business Card Comparison: The Complete Stack

| Card | 0% Period | Ongoing APR | Annual Fee | Key Rewards | Bureau Pull | Reports Personal? |

|---|---|---|---|---|---|---|

| Chase Ink Business Unlimited | 12 months | 16.74–24.74% | $0 | 1.5% unlimited cash back | Experian | No* |

| Chase Ink Business Cash | 12 months | 16.74–24.74% | $0 | 5% office/internet/phone | Experian | No* |

| BofA Biz Advantage Unlimited | 7 billing cycles | 16.74–26.74% | $0 | 1.5%–2.62% cash back | TransUnion | No* |

| BofA Biz Advantage Customized | 7 billing cycles | 16.74–26.74% | $0 | 3% in chosen category | TransUnion | No* |

| Amex Blue Business Plus | 12 months | 16.74–26.74% | $0 | 2X MR points (to $50K) | Experian | No* |

| Amex Blue Business Cash | 12 months | 16.74–26.74% | $0 | 2% cash back (to $50K) | Experian | No* |

| US Bank Business Shield (in-branch) | 18 billing cycles | 16.24–25.24% | $0 | 5% hotel/car rental prepaid | TransUnion | No* |

| US Bank Triple Cash Rewards | 12 billing cycles | 16.24–25.24% | $0 | 3% gas/office/cell/dining | TransUnion | No* |

| Wells Fargo Signify Business Cash | 12 months | 17.49–27.49% | $0 | 2% unlimited cash back | Experian | No* |

* Does not report to personal credit unless delinquent. All five Tier 1 issuers follow this standard for business credit cards.

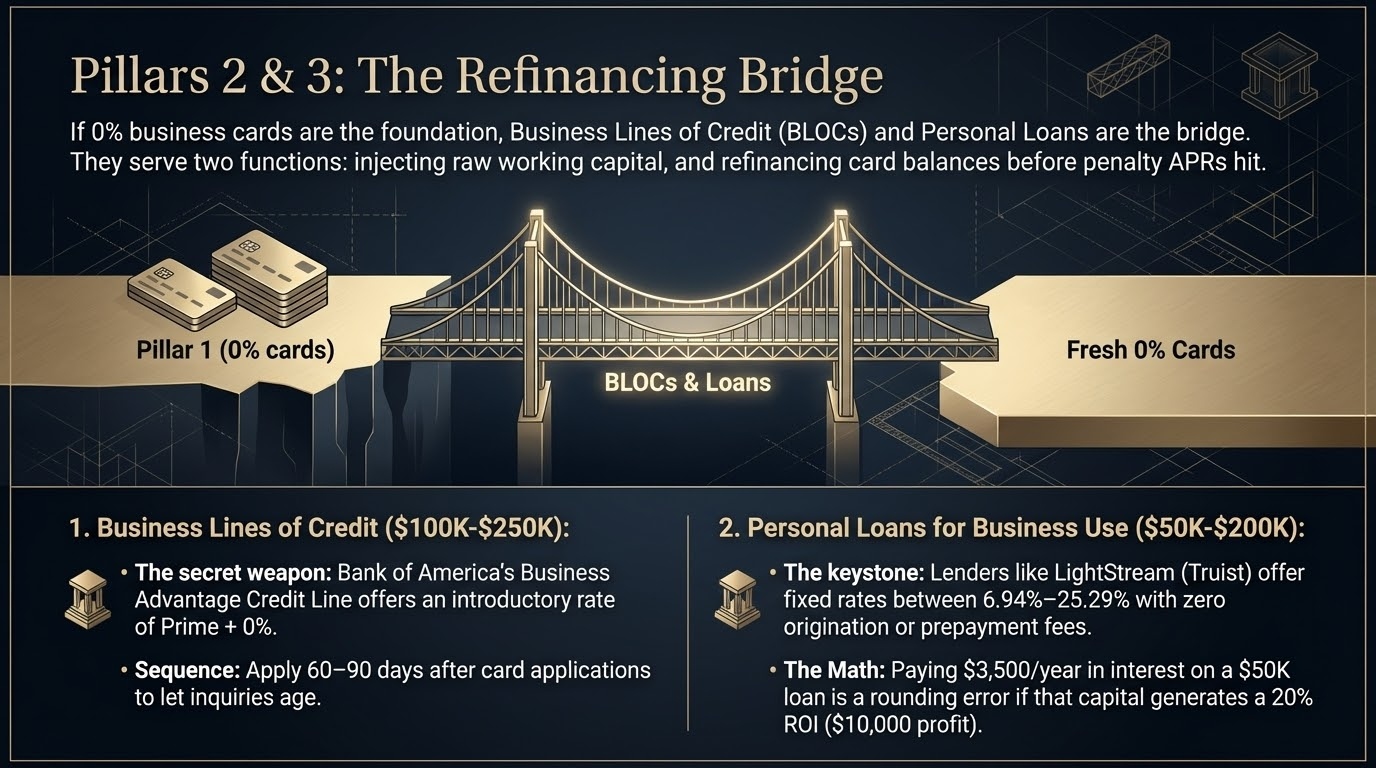

Pillar 2 — Business Lines of Credit ($100K–$250K)

Business lines of credit (BLOCs) are the bridge of the capital stack. They serve two functions: (1) providing flexible revolving capital for operational needs, and (2) acting as the refinancing vehicle when your 0% card periods approach expiration. According to Business.org's unsecured LOC analysis, Tier 1 bank lines of credit offer significantly better terms than fintech alternatives for businesses that qualify.

Bank of America Business Advantage Credit Line

BofA's unsecured Business Advantage Credit Line is the standout in this category. It carries a special introductory rate of Prime + 0% — meaning you only pay the prime rate, with no margin added during the intro period. For a business that qualifies, this is essentially a very low-rate draw-down facility that can be used to bridge card transitions.

Chase Business Line of Credit

Chase offers business lines up to $500,000+ for strong borrowers, though typical approval ranges run $10,000–$250,000 for businesses in the target profile. Per Chase business LOC requirement data, the minimum FICO is 680+ (700+ preferred), with 12–24 months in business and $150,000–$200,000 in annual revenue as baselines. Strong Chase banking relationships dramatically improve both approval odds and credit limits.

Wells Fargo BusinessLine®

The Wells Fargo BusinessLine offers $10,000–$150,000 in unsecured revolving credit. Requirements per Wells Fargo BLOC requirement data: 680+ FICO, 2+ years in business, personal guarantee required from owners with 25%+ ownership. Wells Fargo also offers a Small Business Advantage Line for newer businesses ($5,000–$50,000), but the established borrower should target the full BusinessLine product.

US Bank Business Line of Credit

US Bank offers unsecured business lines of credit for qualifying businesses, with a preference for existing US Bank business checking relationships. Requirements align closely with their card products: 2+ years in business, solid revenue documentation, and an existing business banking relationship. Adding a US Bank BLOC after establishing your card relationship gives you additional draw capacity and extends your capital architecture.

BofA's Prime + 0% introductory BLOC rate is the best-kept secret in business funding. Combined with their Preferred Rewards tiers, you can access six figures at effectively zero cost during the intro period. I execute all three pillars simultaneously — cards, BLOCs, and personal loans in the same application window. Since business cards don't report utilization to personal credit, there's no strategic reason to stagger. The goal is to stack as much capital as possible from Day 1, then manage the refinancing cycle from a position of strength.

| Lender | Min Credit Line | Max Credit Line | Min FICO | Min Years in Biz | Min Revenue |

|---|---|---|---|---|---|

| Bank of America | $10,000 | Varies by profile | 700+ | 2 years | $100,000+ |

| Chase | $10,000 | $250,000+ | 680+ (700+ preferred) | 1–2 years | $150,000–$200,000 |

| Wells Fargo | $10,000 | $150,000 | 680+ | 2 years | Not publicly specified |

| US Bank | Varies | Varies by profile | 680+ | 2 years | Existing relationship preferred |

Free Strategy Session

Not sure which funding products fit your business?

We analyze 20+ lending programs to engineer $50K–$500K+ in capital at 0% interest. Let's build your stack.

Book a Free CallPillar 3 — Personal Loans for Business Use ($50K–$200K)

Personal loans are the final pillar of the capital stack — and frequently the most underutilized. A business owner with 720+ FICO and solid personal income history can access $50,000–$200,000 in fixed-rate, unsecured personal loans through direct lenders. These funds can be deployed into the business without the same restrictions as formal business financing. Per Money.com's personal loan analysis, qualified borrowers can access rates in the 6–12% range — far better than MCA or short-term business loan alternatives.

Personal loans serve two roles in the capital stack: (1) additional deployment capital when cards and BLOCs are fully drawn, and (2) bridge financing when 0% card periods expire before you've rotated the balance into a new 0% product.

LightStream (Truist Bank)

Top PickLightStream, the online lending division of Truist Bank (formerly SunTrust), offers the best combination of loan size, rate, and flexibility in the personal loan market. Per WSJ Buyside's LightStream review, it charges absolutely zero fees — no origination, no prepayment penalty, no late fees — and offers same-day funding for qualifying applications.

Rate Beat Program: LightStream will beat any competitor's rate by 0.10% on identical loan terms — a genuine competitive differentiator. Requires good to excellent credit (670+ FICO minimum, 720+ for best rates).

SoFi Personal Loans

SoFi offers personal loans up to $100,000 with competitive rates and a 0.25% rate discount for debt consolidation with direct payoff. Prequalification is available via soft pull — you can see estimated rates without impacting your credit score.

Note: Verify current SoFi policy on business use of personal loans before application, as policies can change.

Marcus by Goldman Sachs

Marcus offers a streamlined personal loan product with no fees of any kind. Loan amounts are smaller ($3,500–$40,000), making Marcus best suited as a supplemental vehicle rather than a primary capital source.

Personal loans are the bridge that keeps the cycle going. When your 0% periods expire, a LightStream loan at 7% on $50,000 costs approximately $3,500/year in interest — a rounding error on $500,000 in deployed capital. Most business owners have a visceral aversion to personal loans because they show up on personal credit. Get over it. If that $50,000 is generating 20%+ returns in your business, you're netting $6,500+ on the spread even after interest. The math is unambiguous. If you're concerned about your personal credit profile, creditblueprint.org is an excellent resource for understanding how different loan types affect your FICO score before you apply.

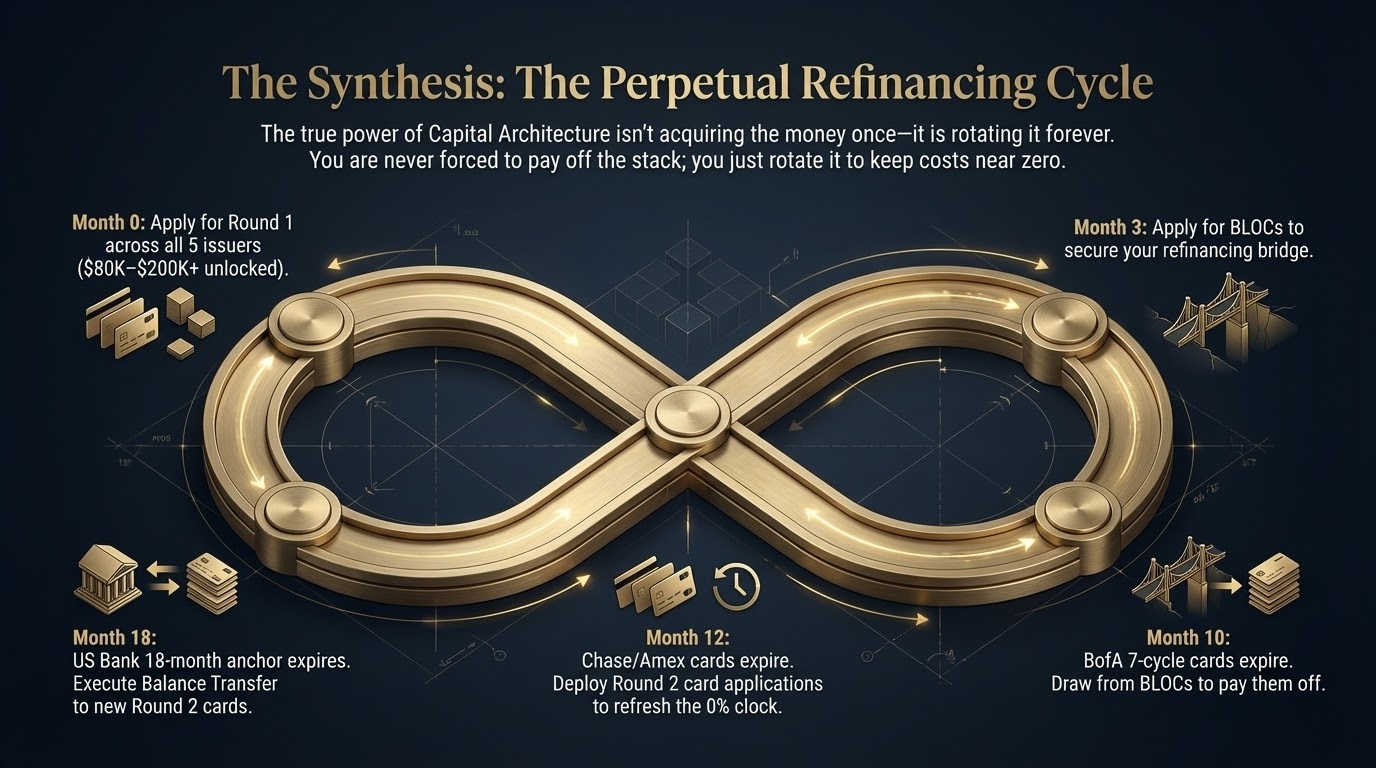

The Refinancing Cycle — How to Keep Capital at 0% Perpetually

The most important concept in this guide is not any individual product — it's the refinancing cycle. This is the mechanism that prevents you from ever paying significant interest on your capital stack. Done correctly, you can maintain $500K+ in deployed capital at near-zero cost indefinitely. Here's how it works in practice:

| Timeframe | Action | Capital Unlocked | Notes |

|---|---|---|---|

| Month 0 | Execute all three pillars simultaneously. Cards: apply across all 5 Tier 1 issuers (US Bank in-branch for 18 months). BLOCs: apply at BofA (Prime + 0%), Chase, Wells Fargo. Personal loans: apply at LightStream, SoFi, Marcus. | $300K–$700K total across all pillars | All three pillars can run in tandem. Business cards don't report utilization to personal credit, so there's no reason to stagger. Stack as much capital as possible from Day 1. |

| Month 1–3 | Deploy capital into business operations. Meet minimum spends for card signup bonuses. Establish payment history across all products. | Capital deployed | Make at least minimum payments on all cards. BLOCs are your refinancing bridge — keep them available for when card 0% periods expire. |

| Month 6–9 | Begin planning Round 2 of card applications. Request credit limit increases on existing cards. | Increased limits | Chase allows new Ink products every 3–6 months. BofA/US Bank prefer 6–12 months between apps. |

| Month 10–11 | 7-cycle BofA cards approaching expiration. Use BLOC draws to pay down BofA balances. | BLOC funds BofA payoff | Don't let any 0% period expire with a large balance and no plan. |

| Month 12 | 12-month 0% cards (Chase, Amex, WF Signify) approaching expiration. Deploy Round 2 card applications. | New 0% capital | New cards refresh the 0% clock. Transfer existing balances to new 0% cards where possible. |

| Month 13–15 | Round 2 cards funded and deployed. Old balances rotated to new 0% instruments. | Full stack refresh | Effective interest rate on total stack: still near 0%. |

| Month 18 | US Bank Business Shield (18-month anchor) approaching expiration. By now, Round 2 cards have new 0% periods. | Cycle complete | Apply for Round 3 US Bank products or balance transfer to new cards. |

| Month 18–24+ | Perpetuate the cycle. The capital stack never fully costs interest if managed proactively. | Ongoing | Year 2+ can add new issuers (Elan/TCM Bank products) to expand capacity further. |

Every 0% period needs an exit plan before it expires — not after. If a $40,000 balance on a Chase Ink card is about to start accruing 22% APR, that's $8,800/year in interest you were supposed to avoid. The exit options are: (1) full payoff from business cash flow, (2) BLOC draw to pay the card, (3) balance transfer to a new 0% card, or (4) personal loan consolidation. Plan the exit on Day 1, not Day 360.

Balance Transfer Strategy

The US Bank Triple Cash Rewards card includes 0% on balance transfers for 12 billing cycles — making it a dual-purpose product. When a competitor card's 0% period is expiring, transferring the balance to a US Bank card resets the clock at 0% (minus any balance transfer fee, typically 3–5%). The math: a 3% fee on a $30,000 balance is $900 to buy another 12 months of 0% — versus $6,600+ in interest at 22% APR for a year. The arbitrage is obvious.

As your stack matures and you build relationships with additional Tier 1 issuers, Elan Financial Services products (typically TransUnion) and TCM Bank products (typically Experian) can extend your capacity further. Elan issues cards for numerous regional banks and credit unions, while TCM Bank specializes in retail co-branded cards — both providing additional 0% balance transfer capacity from a different bureau profile than your five primary issuers.

Expert Guidance

Have questions about your funding options?

Get a personalized capital strategy from our team. We'll identify which products you qualify for and the optimal order to apply.

Book a Free CallThe Bankability Prerequisite

Everything in this guide depends on being "bankable" — having a profile that qualifies for Tier 1 bank products. This isn't an arbitrary gatekeeping concept. It's a specific, measurable set of criteria that banks use to evaluate risk. The good news: if you're running an established business with real revenue, you likely already meet most of these criteria. The bad news: most business owners don't know which boxes they're failing to check.

What "Bankable" Means

The 90-Day Pre-Stack Optimization Checklist

If you have 90 days before you plan to start stacking, here's exactly what to do to maximize your position:

Most business owners don't realize that timing matters more than credit score when it comes to maximizing approval limits. Apply for all cards at the same bank on the same day — this consolidates their hard pulls and prevents the bank from seeing competing applications at sister products as a risk signal. Also: the best time to apply for new credit is before you need it. If you're waiting until your business has a cash flow crisis to start stacking, you've already lost. Build the infrastructure when you're strong, so you can deploy when opportunity arrives.

Credit Reporting Impact — The Full Picture

One of the most misunderstood aspects of business credit stacking is how different products interact with your personal credit profile. The short version: all five Tier 1 issuers' business cards do NOT report to personal credit unless delinquent. The nuances that matter are in the BLOCs and personal loans — those do appear on your personal credit report.

| Product | Reports Personal Credit? | Hard Pull? | Bureau(s) Pulled | Impact on Personal FICO? |

|---|---|---|---|---|

| Chase Ink Business Cards | No (unless delinquent) | Yes | Experian (typically) | Minimal — only inquiry impact |

| BofA Business Advantage Cards | No (unless delinquent) | Yes | TransUnion (typically) | Minimal — only inquiry impact |

| Amex Blue Business Cards | No (unless delinquent) | Soft then hard on approval | Experian | Minimal — only inquiry impact |

| US Bank Business Cards | No (unless delinquent) | Yes | TransUnion (typically) | Minimal — only inquiry impact |

| Wells Fargo Business Cards | No (unless delinquent) | Yes | Experian | Minimal — only inquiry impact |

| Business Lines of Credit | Yes (personal guarantee) | Yes | Varies by bank | Moderate — installment/revolving impact |

| Personal Loans (LightStream, SoFi, Marcus) | Yes (personal loan) | Yes | Varies by lender | Moderate — installment tradeline |

Managing Utilization Across the Stack

Utilization management is the ongoing discipline of the capital stack. Here's the framework:

- → All Tier 1 business cards (Chase, BofA, Amex, US Bank, Wells Fargo): Carry whatever balance makes business sense. None of these issuers report business card activity to personal credit unless the account becomes delinquent. The only personal credit impact is the initial hard inquiry at application.

- → Business Lines of Credit: These appear on personal credit due to the personal guarantee, but they function as revolving credit. Keep reported BLOC balances below 30–50% of the credit limit if possible — or pay to zero before the monthly reporting date if a FICO-sensitive event is upcoming.

- → Bureau-specific strategy: Experian: Chase (2 cards, 1 hard pull) + Wells Fargo (up to 2 cards) + Amex (soft pull if existing personal relationship). TransUnion: BofA (up to 5 cards, all within 30 days = 1 inquiry) + US Bank (in-branch for 18 months). Equifax: credit unions (use NCUA Credit Union Locator), Truist, and KeyBank for additional capacity on a third bureau.

The Math — Why This Strategy Works

The fundamental economics of the capital stack are compelling. Let's work through the numbers at several scenarios:

Scenario A: $500K at 0% — The Pure Arbitrage

Capital Stack Cost

*BLOC at Prime + small margin after intro period. Prime rate varies.

Deployed at 20% Business ROI

Scenario B: The Opportunity Cost of NOT Stacking

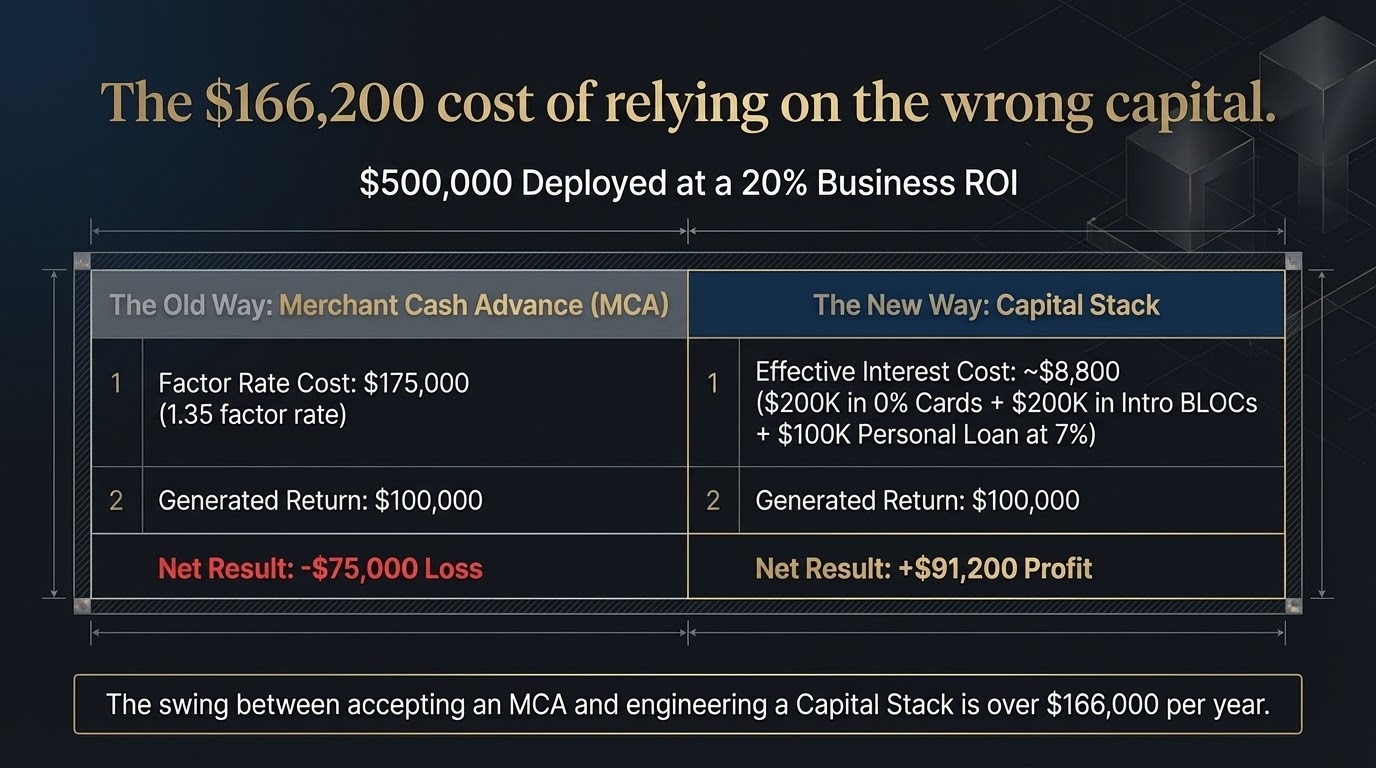

The question isn't just "what does the capital stack cost?" — it's "what is the cost of not having it?" Consider a business owner who deploys an MCA instead:

MCA Financing — $500K

Capital Stack — $500K

Swing between MCA and stack: $166,200 per year

This is not a hypothetical. According to LendingTree's business loan rate data, small businesses that accept MCA financing are frequently paying effective APRs of 40–150%+ — and many qualify for Tier 1 bank products at 0% but simply don't know the strategy. The gap between what's available and what most business owners access is genuinely staggering.

Even in a scenario where you're paying 7–12% on some of the capital stack (personal loans, BLOCs after intro periods), the spread between your capital cost and your business ROI — if your business is generating 20%+ returns on deployed capital — is enormous. This strategy is most powerful not as a one-time funding event, but as a permanent capital infrastructure that gives your business access to expansion capital at near-zero cost, year after year.

Don't Navigate This Alone

Let us engineer your capital stack

The sequencing, bureau strategy, and timing that maximize your capital access have taken us years to optimize. Let's build your architecture together.

Book a Free CallCommon Mistakes That Kill a Capital Stack

These are the mistakes that turn a $500K capital stack into a $150K one — or worse, into a credit profile that can't get approved at all.

Mistake #1: Applying to All Issuers on the Same Day Without Bureau Strategy

Applying to all five issuers without a bureau strategy creates unnecessary inquiry damage. The fix: Experian round — apply for both Chase Ink cards (1 inquiry), both Wells Fargo cards, and Amex (soft pull if existing personal card). TransUnion round — apply for up to 5 BofA cards (all combine into 1 inquiry within 30 days) and US Bank cards. Equifax round — credit unions, Truist, KeyBank for additional capacity. After each round, pause to remove inquiries before the next cycle.

Mistake #2: Ignoring Utilization Management After Funding

Getting approved for $250,000+ across all three pillars is the goal — but deploying all of it into the business without a repayment plan is where things go wrong. The fix: Deploy capital strategically. Fund the highest-ROI business needs first. Always have a clear plan for how each dollar gets repaid or refinanced before the 0% periods expire.

Mistake #3: Not Establishing Bank Relationships Before Applying

Walking into a bank as a new customer and immediately applying for a business credit card is the single most common application mistake. Banks heavily weight existing relationship depth in their underwriting. A business with 90+ days of business checking history and healthy deposit balances will consistently receive higher limits and better terms than a brand-new relationship. The fix: Open all five bank accounts 90 days before your first applications. Period.

Mistake #4: Applying Online for US Bank Instead of In-Branch

This is so critical it deserves its own mistake entry. The difference between US Bank's online application (12 billing cycles of 0%) and the in-branch application (18 billing cycles) is six months of interest-free capital. On a $30,000 credit line at 20% APR, that's $3,000 in saved interest. The fix: Walk into a US Bank branch. Ask the banker specifically for the Business Shield Visa or Business Platinum with the 18-billing-cycle promotional rate.

Mistake #5: Not Having an Exit Plan for Each 0% Period

The single most expensive mistake in the entire framework. A business owner who deploys $200,000 in 0% cards, forgets about the expiration dates, and then suddenly faces 20-25% APR on six-figure balances has completely negated every advantage of the strategy. The fix: On Day 1 of any 0% product, set a calendar reminder for Month 10 (two months before expiration). Plan your exit then, not later. The BLOCs you opened in Month 3 exist specifically for this purpose.

Mistake #6: Treating This as a One-Time Funding Event

The power of the capital stack is the perpetual refinancing cycle — not the initial funding. Business owners who use the strategy once, pay it off, and never return to it have missed 90% of the value. The fix: Think of the capital stack as permanent infrastructure, not a one-time loan. Maintain your bank relationships, keep your FICO above 720, and run the refinancing cycle continuously. The annual cost of the infrastructure (time, minimal interest) is far less than the value of having $500K in deployable capital available on demand.

Frequently Asked Questions

Can I really get $500K in unsecured business funding without collateral?

Yes — for qualified businesses with 720+ FICO, 2+ years in business, and $1M+ in revenue, stacking $500K+ in unsecured capital across 0% APR business credit cards, business lines of credit, and personal loans is a well-documented strategy used by established business owners. It requires strategic sequencing and a bankable profile, but the capital is real, accessible, and genuinely unsecured. Per Bankrate's analysis of unsecured business loans, unsecured capital is broadly available to creditworthy borrowers — most simply don't know how to stack multiple products effectively.

Won't applying to multiple banks at once hurt my credit score?

Multiple applications do trigger hard pulls, but the impact is manageable with proper bureau strategy. Chase and Wells Fargo hard-pull Experian — but Chase treats both Ink applications on the same day as a single inquiry (2 cards, 1 pull). Amex pulls Experian too, but if you hold an existing personal Amex card for 3+ months, business card applications are typically soft pulls — no hard inquiry. On the TransUnion side, BofA combines all applications within a 30-day window into a single inquiry and allows up to 5 business cards (the 2/3/4 rule doesn't apply to business). US Bank also pulls TransUnion. For a third bureau, Equifax-pulling issuers like Truist, KeyBank, and credit unions give you additional capacity without touching Experian or TransUnion. After each round, pause to remove inquiries before starting the next cycle.

How long does it take to build a $500K capital stack?

For a fully prepared borrower with existing Tier 1 bank relationships, all three pillars can be executed simultaneously. Card applications can happen in a single day, with approvals and delivery within 7–14 days. Personal loan funding through LightStream can happen same-day or next-day. BLOC approvals typically take 1–3 weeks. Since business cards don't report utilization to personal credit, there's no strategic reason to stagger — stack all three pillars at once. Realistically, a well-prepared business owner can have $300,000–$500,000+ in place within 30 days of starting. If you're starting from scratch (no bank relationships yet), add 90 days for relationship establishment — the total timeline becomes 4–5 months. This is why the 90-day prep work described in the Bankability section is so valuable.

What if my 0% period expires before I can pay it off?

This is where the refinancing cycle saves you. The US Bank Business Shield at 18 billing cycles gives you the longest runway. When shorter 0% periods approach expiration, you have four options: (1) pay the balance from business cash flow, (2) draw from your BLOC to pay the card balance (the BLOC serves as the bridge), (3) apply for a new 0% balance transfer card from the same issuer — most issuers will approve a second card after 6–12 months, and (4) consolidate at low fixed rates via a personal loan from LightStream or SoFi. The key principle: never let a 0% period expire without a plan. If you set a reminder 60 days before expiration, you'll always have time to execute one of these options.

Do I need banking relationships at all five Tier 1 banks?

You don't need all five — you can build a strong stack with 3–4 relationships. However, having all five maximizes your total available capital and gives you the most flexibility in the refinancing cycle. At minimum, prioritize Chase (best overall approval limits for established businesses), Bank of America (best BLOC introductory rate), and US Bank (18-month 0% anchor via in-branch application). Wells Fargo adds incremental Experian-side capacity (up to 2 business cards), and Amex adds Experian-side capacity with the soft-pull advantage for existing cardholders. Start with your existing banking relationships — the issuer where you already have a business checking account should be your first application.

What about SBA loans versus credit stacking?

SBA loans offer larger amounts (up to $5M for SBA 7(a)) and longer terms at competitive rates — but they're slow (60–120 days to fund), require extensive documentation, often require collateral for larger amounts, and the approval process is rigid. Credit stacking is faster, more flexible, and can be deployed in tranches as opportunities arise. The two strategies are genuinely complementary, not competing. Use SBA loans for large capital expenditures, real estate, or equipment with long useful lives. Use credit stacking for working capital, inventory, marketing campaigns, and opportunistic deployment. If you're in the target profile for this guide ($1M+ revenue, 720+ FICO), you likely qualify for both — and should have both strategies in your toolkit.

How does building a credit stack affect my ability to get a mortgage?

Business cards from all five Tier 1 issuers — Chase, BofA, Amex, US Bank, and Wells Fargo — do NOT report to personal credit unless delinquent, meaning they won't impact your mortgage DTI calculation or personal credit utilization. Business lines of credit appear on personal credit due to the personal guarantee, and personal loans will show on your personal credit report. If a mortgage is on the horizon within 12–18 months: (1) pay down BLOC balances before the mortgage application, (2) time any personal loans well in advance to allow the inquiry impact to age, (3) let all new accounts season for at least 12 months before applying for the mortgage, and (4) keep card accounts in good standing since delinquency would trigger personal reporting. Mortgage underwriters want to see a stable credit profile — a stack of brand-new accounts applied for simultaneously can trigger additional scrutiny.

Is credit stacking legal?

Absolutely. Applying for multiple business credit products is entirely legal and is standard practice among well-capitalized businesses. There is no law or regulation limiting the number of business credit cards or lines of credit a business can hold. Banks set their own internal policies (such as Chase's 5/24 rule for personal cards), which is why strategic sequencing and bureau management matter — but there is nothing legally problematic about building a diversified credit portfolio across multiple Tier 1 institutions. The strategy described in this guide is used by businesses of all sizes, including publicly traded companies that maintain multiple revolving credit facilities across different bank relationships.

Continue Your Funding Education

Chase Ink Business Cards: The Complete Guide

Read Guide Business LendingBusiness Lines of Credit: Complete Guide to Tier 1 BLOCs

Read Guide Credit StrategyThe Bankable Blueprint: How to Build a Bank-Ready Business Profile

Read Guide Business CardsAmerican Express Business Products: Complete 2026 Guide

Read GuideSchedule Your Free Consultation

Build Your Capital Stack

Tell us about your business and funding goals. We'll map out a custom capital architecture strategy — identifying which products to apply for, in what order, and how to maximize your total accessible capital.